4.1. 1D trend filtering#

4.1.1. Introduction#

In some real world applications, we want to recover the underlying trend of a series of data (e.g., time series), that is, smooth a noisy time series. For example, we can indentify the trend of the US stock market by filtering the daily return data of S&P 500.

Mathematically, we aim at fitting a time series \(\mathbf{y}\in\mathbb{R}^n\) with a piecewise constant vector \(\mathbf{\beta}\in\mathbb{R}^n\).

Note that, the piecewise linearity of a vector can be characterized by the sparsity of its first order difference \(\beta_j-\beta_{j-1}, j=2, \cdots,n\).

For \(\ell_1\)-type methods, such as fuesed lasso [1] [2], this kind of sparsity is obtained by penalizing the \(\ell_1\) norm of the first order difference. Specifically, they solve the following problem

where \begin{align*} \mathbf{D} = \begin{bmatrix} 1 & -1 & 0 & \cdots & 0 & 0\\ 0 & 1 & -1 & \cdots & 0 & 0\\ \vdots & \vdots & \vdots & & \vdots & \vdots\\ 0 & 0 & 0 & \cdots & 1 & -1\\ \end{bmatrix}. \end{align*} That is, we expect that the successive jumps \(\beta_j-\beta_{j-1}\) are sparse.

Different from the Lasso-type methods, skscope is a \(\ell_0\)-type algorithm.

Therefore, we can solve this problem by considering the following sparse optimization problem

However, this sparse optimization can not be solved by skscope since it expects a direct sparse parameter (e.g. \(\mathbf{\beta}\)) rather than a linear transformed one (here \(\mathbf{D\beta}\)).

Instead, we reparametrize \(\mathbf{\theta}=\mathbf{D\beta}\), that is, we directly let the sparse successive jump be the parameter optimizaed by skscope. Then, we represent \(\mathbf{\beta}\) with \(\mathbf{\theta}\) as \(\mathbf{\beta}=\mathbf{Q\theta}\) where \begin{align*}

\mathbf{Q} =

\begin{bmatrix}

1 & 0 & 0 & \cdots & 0 & 0\\

1 & 1 & 0 & \cdots & 0 & 0\\

\vdots & \vdots & \vdots & & \vdots & \vdots\\

1 & 1 & 1 & \cdots & 1 & 1\\

\end{bmatrix}.

\end{align*}

Therefore, we can solve the following sparse optimization via skscope directly

4.1.2. Implementation#

Under the above formulation, we define the main function trend_filter as follows.

Note that, with our reparametrization, the expected piecewise linear vector is directly represented with a sparse params via the function jnp.cumsum(params).

Then, we minimize the mean square loss jnp.mean(jnp.square(y - jnp.cumsum(params))) with the user-defined sparsity level \(k\).

Lastly, we ouput the trend of original data \(y\).

[1]:

import numpy as np

import jax.numpy as jnp

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')

from skscope import ScopeSolver

import warnings

warnings.filterwarnings('ignore')

[2]:

def trend_filter(y, k):

y = jnp.array(y)

p = len(y)

# we hope the jump is sparse, thus defining params

# to be the successive increment of y, i.e.

# y can be represented as the cumsum of params

def custom_objective(params):

return jnp.mean(jnp.square(y - jnp.cumsum(params)))

solver = ScopeSolver(p, k)

theta_hat = solver.solve(custom_objective)

y_hat = jnp.cumsum(theta_hat)

return y_hat

4.1.3. Synthetic data example#

In this example, we generate \(\mathbf{y}\) as a \(500\)-step random walk with normal increment.

[3]:

# random walk with normal increment

def gen_normal(n_step=500):

x = np.random.randn(n_step) / np.sqrt(n_step)

x = np.insert(x, 0, 0)

y = np.cumsum(x)

return y

np.random.seed(0)

y = gen_normal(500)

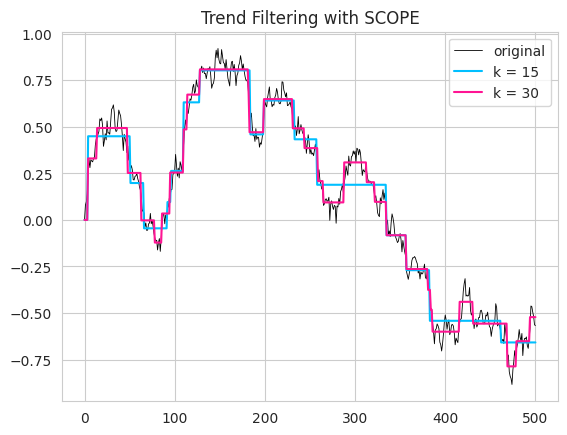

Here, we consider two different sparsity level \(k=15, 30\) and visualize the result in the following figure.

The resulted estimator \(\widehat{\mathbf{y}}\) is a piece-wise constant line and more jumps exist if \(k\) is larger (see the blue and pink lines in the following figure).

Original data \(\mathbf{y}\) is zigzag due to the existence of noise. While the smoothed line \(\widehat{\mathbf{y}}\) is more smooth and it better exhibit the underlying trend of \(\mathbf{y}\).

[4]:

k_list = [15, 30]

color_list= ['deepskyblue', 'deeppink']

sns.lineplot(y, label='original', linewidth=0.6, color='k')

for i in range(len(k_list)):

k = k_list[i]

yk = trend_filter(y=y, k=k)

sns.lineplot(yk, label=r'k = {}'.format(k), color=color_list[i])

plt.legend()

plt.title('Trend Filtering with SCOPE')

plt.show()

No GPU/TPU found, falling back to CPU. (Set TF_CPP_MIN_LOG_LEVEL=0 and rerun for more info.)

4.1.3.1. Reference#

[1] Tibshirani R, Saunders M, Rosset S, et al. Sparsity and smoothness via the fused lasso[J]. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 2005, 67(1): 91-108.

[2] Kim S J, Koh K, Boyd S, et al. \(\ell_1\) trend filtering[J]. SIAM review, 2009, 51(2): 339-360.